Latest Activity...

It's Wednesday - cheers on getting halfway through the week! Some major updates came out this past week, and we're excited to finally be about to talk about them. In total, there were 17 updates for the past week, so we better get right to it.

For a long time, one of the biggest complaints about our Hosted Websites has been that they look too plain. While fast and powerful, our Hosted Websites all look the same - meaning your website looks the same as every other OwnerRez client's website. We are on a mission to change that with a lot of upcoming changes and new features for hosted websites.

The first major update was to the header/menu area. We just released a big overhaul that allows you to greatly customize the header & menu area including multiple lines, sections, different kinds of links and buttons and different styles on desktop versus tablet versus mobile. You are now in control of this area and its design.

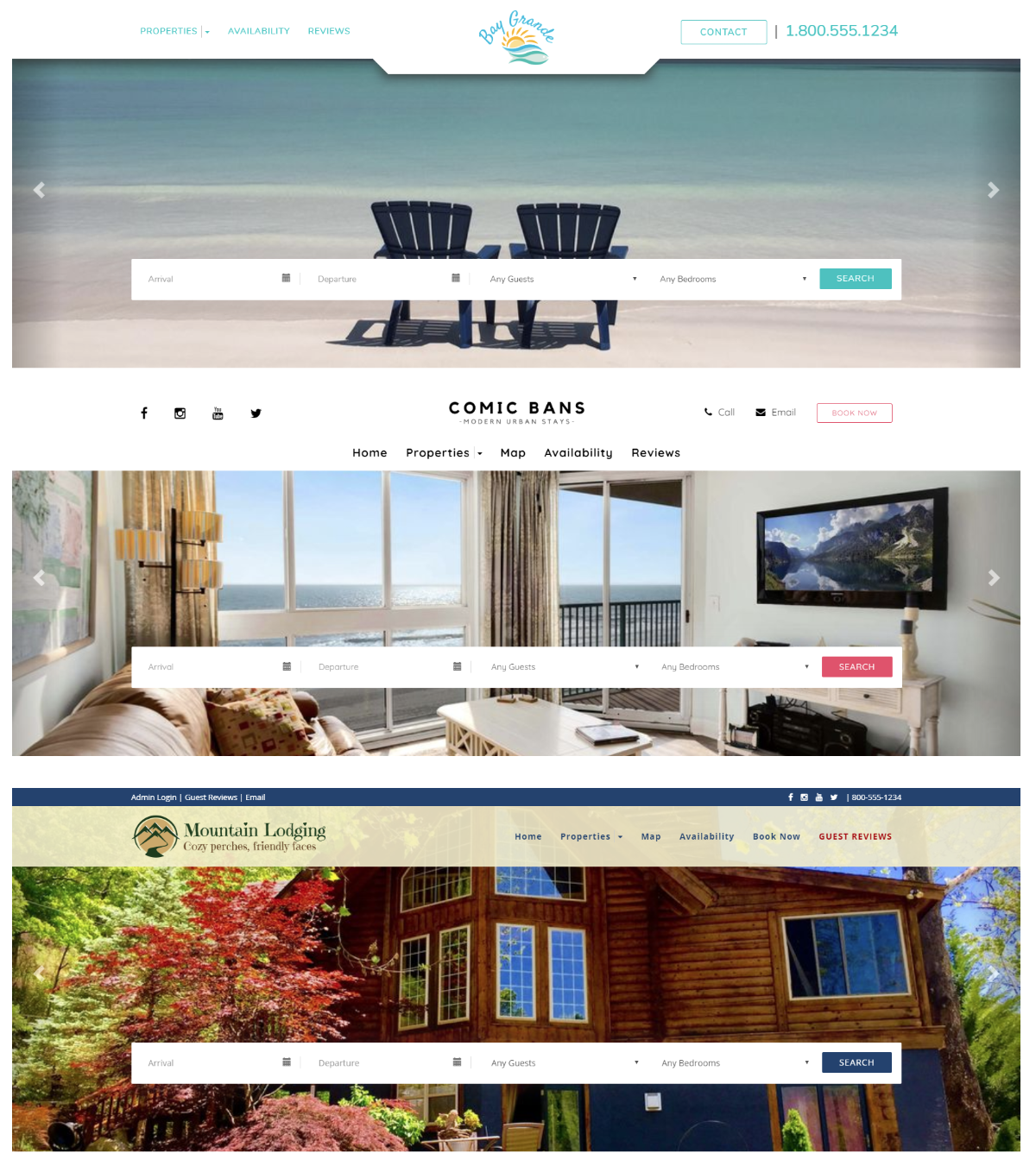

To demonstrate what can be done, and get you started with different ideas, we also added a predefined template selector that shows three styles and lets you quickly apply one to your header. Here's a quick peek at those predefined templates:

Notice specifically how the headers look - notice where the menus are, other links, logo placement, etc. These templates simply move the header lines and sections around and put your logo and links in different areas so that you get an idea of how headers work. You can add additional styling as well both on the line and section level.

We also put together a 10 minute video walking you though how headers work, so give that a look. Some great material here!

We know many of you will have questions about the new header area, but please watch the video first before sending an email. We're happy to help as always!

If there's a website idea or template you'd like to copy - such as someone else's in the industry - and can't figure out how to do it with our new header area, let us know. Our goal is to support a wide range of header and menu layouts such that most types of designs are possible from a structural standpoint.

To aid with better website design and customization, we also added support for Google Fonts. If you're not familiar with it already, Google Fonts is an online platform that Google created which manages and publishes fonts for designers and website owners to use free of charge. Learn more about it on the Google Fonts website or browse hundreds of fonts directly. There are almost 1,000 fonts available to use completely free of charge.

OwnerRez websites now directly support all these fonts.

OwnerRez websites now directly support all these fonts.

If you have an OwnerRez hosted website, click the Fonts & Colors tab at the top, find any font field and you'll see a "type in Google font" option. Click that and then type in the name of the Google Font in the box that appears to the right. Save and you're done!

Over on the channel management side, we've been working on adding some new API integrations. As our clients know, we are very selective about integrating with new channel APIs because it takes a lot of work to build and maintain those integrations, and we have to be careful how we allocate resources. Frankly, many OTA's simply aren't worth the investment given how little vacation rentals actually book on those sites.

But some of them are! We're happy to announce that we just released beta support for Houfy as a new API integration. Houfy is near and dear to many of our clients' hearts because Houfy promotes direct bookings without platform fees and they don't restrict communication.

While Houfy may not currently send you the same volume of traffic that other channels do, we're hoping that, over time, our clients can build volume on sites like Houfy and strengthen the #DirectBooking ecosystem. We are strong advocates of the #DirectBooking movement and integration with Houfy is a part of that. By working with the Houfy team to provide direct API integration, you can keep your listings up to date on Houfy without any extra work.

Please note that our Houfy integration is a limited beta. The integration does not yet support everything you may be used to with Vrbo or Airbnb integrations because we are still in the process of fully fleshing out the integration with the Houfy dev team. After connecting, you may need to manually update some pricing or others things on the Houfy side - those things should be supported by the API in the future. Basic listing content and availability is already supported and your availability will update dynamically on the Houfy side. We are still in the process of updating our support docs, so we appreciate your patience!

Last but not least, we now support Schlage door lock when using the RemoteLock door lock integration. If you have Schlage door locks, you can now sign up with RemoteLock and then connect that RemoteLock account to OwnerRez and we'll set your door codes automatically.

When it comes to rates and rules, OwnerRez is a lot more flexible than the channels are. You can customize our surcharges into pretzels, targeting only certain time periods or other custom criteria. The problem is that this creates conflicts between what we support and what gets pushed to the channels. We typically have a "best guess" approach that maps our more-flexible options against their less-flexible ones. To aid with this, we recently changed fee criteria and minimum night checks to go on arrival date only to align with channel criteria. While this means the fee and rules won't "split across" the booking like it does with OwnerRez direct bookings, it will also reduce confusion in what the guest (and you) expect on the channel side.

The new Airbnb Messages inbox has been tweaked to wrap messages, load more quickly and some other minor things. Keep sending your feedback on that. The inbox is a prototype of some great things to come.

When creating or changing website content, you often want to save something and then preview the changes in a different tab or window. It was irritating to save and be redirected away and have to click several times to come back every time. We added a "Save & Close" and "Save" button on website pages so that you can save while staying where you are.

Similarly, we noticed that website pages typically showed a lot of general settings at the top and the body content was pushed way down the page. General page settings aren't changed as often as body content, so we moved those page settings to other tabs and made the body content front and center.

Confused about the fireplace icon that we used when showing the fireplace amenity? We were too. It kind of looked like a smoking sign which gave off a very different impression than desired. We changed the fireplace icon to something that looks a lot more like a campfire.

The rate table widget was also changed quite a bit to promote clarity and information. We are now only calculating contiguous rates when analyzing date ranges. We no longer calculate longer rates for the table if the rates lap over into other seasons. And we are only showing the discount percentage if there is one.

Sorry, Internet Explorer 11, but you are no longer welcome at OwnerRez. We removed access for IE 11 browsers entirely on the client side (guests can still use it). To be clear, this is Internet Explorer and not Edge. Edge is a great browser and very much supported. Let us know if this puts you in a bad way, but it was time to be done with Internet Explorer for good since it is now an obsolete browser. Feels like the end of an era, doesn't it.

Duplicate Airbnb new booking emails. We removed the duplicate sending of Airbnb new booking emails if cancelled again.

TripAdvisor API incorrect LOS discounts. If you were API integrated with TripAdvisor, you might have noticed that LOS (weekly, monthly) discounts were calculating incorrect. This has now been fixed.

Line Item Summary report incorrectly grouping other surcharges as not rent. This was fixed.

Airbnb weekly/monthly rates. If there were other LOS rules, we were sometimes skipping the weekly and monthly discounts for Airbnb. This has now been fixed.

Vacation rentals are a lucrative business that is constantly changing and adapting to the times. Covid has brought opportunity to purchase properties at a bargain. We would like to hear what your plans are for expanding your business. What size of business would you like to get to and how many properties are you planning on adding?

(make sure to scroll to the bottom and click the Submit button)

If the survey form didn't load, use this link instead:

Do you plan on expanding your vacation rental business?

After I accept the booking I ask guests via Airbnb to provide their email address so I can send them rental agreement. 99% of the time they do and if they don't I use the Airbnb provided email address. After that I still get their email address as mentioned when they sign the rental agreement.

When I click on link to opt-in to the promotion for 7 day discount, I just go to a page that has a couple standing beside an open air dining table. I don't see anywhere to opt-in? Am I missing something?

Winding down Airbnb. Every time they do some stupid #$%* I think I cannot hate them more, yet each time they prove me wrong and outdo themselves. I sincerely wish they went back to renting illegal sublets, basement rooms and attics and butted out of traditional vacation rentals that they obviously have 0 clue about.

I don't see how this would work for us. We send out our Welcome Note with Activity Guides as an automatic trigger with airbnb bookings, followed by a RA. Now, we aren't even going to be able to proxy email our airbnb guests?

Good grief. Doesn't the Professional Hosting Tool require a different OR subscription? And if there's a secret way around this new edict, what is the purpose?

Ken T said:

I'm glad it looks that way, but that's an illusion. Airbnb has never sent real email addresses, just the fake proxy one.We recommend configuring an automatic email template and trigger asking guests to sign your rental agreement. As part of this process, they're asked for their real email address, which is then recorded. I think that's what you're seeing.

https://www.ownerrez.com/support/articles/airbnb-request-for-contact-info-real-email-address-and-signed-renter-agreement

Are you sure about this? I regularly see (but not always) the guests real email address on airbnb reservations made via API. I don't update it myself, so it's coming from somewhere.

I'm glad it looks that way, but that's an illusion. Airbnb has never sent real email addresses, just the fake proxy one.

We recommend configuring an automatic email template and trigger asking guests to sign your rental agreement. As part of this process, they're asked for their real email address, which is then recorded. I think that's what you're seeing.

https://www.ownerrez.com/support/articles/airbnb-request-for-contact-info-real-email-address-and-signed-renter-agreement

I'm curious about how this affects API connection with Airbnb. We seem to get the clients real email address now during the data transfer with API. Rick@kismetprop30a.com

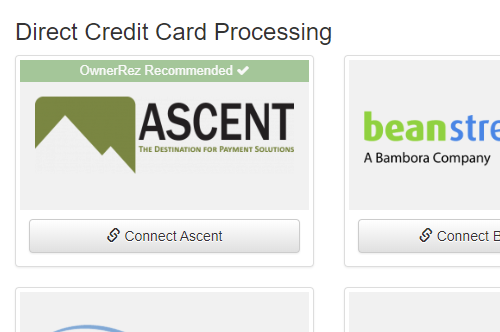

We are pleased to announce we have partnered with ASCENT to provide payment processing for vacation rentals.

About Ascent:

ASCENT provides payment regulation expertise, modern and innovative technology programs, customized chargeback and support services for the top reservation software providers and the leading property managers in the alternative lodging space. ASCENT was the first processor in the industry, more than 20 years ago, to integrate gateway/processing within reservation software and to develop security measures specifically for Vacation Rentals. ASCENT remains independently owned and focused on providing customized programs property managers need to grow and protect their clients’ businesses.

ASCENT sets you up as the Merchant of Record (MOR), so a property manager’s funds are FDIC ensured every step of the way, from the guest’s card to the merchant’s bank account. Being MOR gives the most freedom to property managers to set their own policies and practices. This process may require additional documentation, but once a completed application is received, typically an account can be set up within 14 business days.

ASCENT is dedicated to saving their clients’ money, which they do in many ways, including offering interchange pass thru pricing. They have always utilized this pricing program because it is the most transparent model for merchants to know exactly what they are paying for each card type, along with the service fees, dues, and assessments that are passed along by the banks.

Independent sources agree that this pricing program allows merchants to achieve optimal interchange rates, better than other pricing programs like flat rate or tiered. US-based companies get a free competitive analysis at 888-721-9301 info@ascentprocessing.com www.ascentprocessing.com, or OwnerRez clients click here.

Thanks for all your help!

trying to remember and Sending my automated emails manually because the time that are being sent does not work for me. It would be awesome if we can customize what hour of the day these emails are being sent.

By API expert, do you mean developer/engineer? If so, we may be looking for another dev in 6 months or so, but first the CSR and QA side.

Thanks for the input, Ragip! We have a lot in store of messaging, so keep the feedback coming.

Here you go Ken, your software is so good I really don't do anything but check for messages and lookup information on bookings.

Good News! It's Friday!

Oh boy…. Airbnb will no longer be giving out proxy/double-blind email addresses soon. In other words, the "guest.airbnb.com" email address that used to come along with the booking is going to disappear and they’re going to expect you to do all messaging through Airbnb only.

Couple interesting notes here:

There is also a mention that requesting guest contact info violates the "Off-Site Policy" but that is only prior to booking. We highly encourage all hosts to get POC information and a real renter agreement after the guest books!

Another interesting Airbnb thing we came across… Between now and mid-August, Airbnb will showcase a “Discounted Nearby Stays” banner on its home page, directing guests to a dedicated landing page featuring local getaways for domestic travelers.

People are looking for affordable options close to home, so Airbnb created a promotion specifically designed to focus on short lead time to help fill occupancy rates and help you capture that demand. Airbnb sent a company wide email Thursday, to Airbnb guests in Florida - so it is definitely valuable to opt in ASAP. Your listings will be visible to these guests when they search by offering a 10% discount. Note that the Airbnb site refers to "7 consecutive dates" but the discount can apply to any number of nights.

Here's how it works:

Am I listed on HomeAway? Am I listed on VRBO? What about VacationRentals.com or Abritel? Am I listed on all of them? Are they the same? HomeAway/VRBO have decided to clarify this and starting next month, HomeAway website users will be redirected to Expedia's Vrbo vacation rental platform.

To be clear, that’s pronounced "verr-bo" which Expedia continues to reiterate. Make sure to spell it “Vrbo” and not VRBO too. 🤓

While users of the HomeAway app will be prompted to download the Vrbo app, any existing rental bookings will remain unchanged, and all HomeAway logins will transfer over to Vrbo. According to Expedia, the consolidation effort "means more resources can be dedicated to marketing, engineering and customer support for Vrbo," which the company has positioned as its flagship vacation rental product.

Airbnb Messages inbox is an awesome feature. Thanks. I look forward to its extensions including at least the property name, and a link to the Ownerrez reservation.

Any plans for a similar inbox for VRBO.

My husband is an API expert. Let me know when you need some help in that area and I will give him a nudge :)

Here at OwnerRez we know how much work goes in vacation rentals. It can take multiple people to manage all the intricacies of the business. We'd love to know how many properties you have, what size staff it takes to run and how you handle cleaning/maintenance. Let us know below.

(make sure to scroll to the bottom and click the Submit button)

If the survey form didn't load, use this link instead:

What repetitive task takes you the most time in OwnerRez each week?

Happy Hump Day! Let's talk updates.

Last week we were short-staffed and had a bunch of things in transition, so there was no Wednesday update. This week, we'll discuss the 17 updates that occurred collectively over the past two weeks, most of which were enhancements and bug fixes.

We now support Ascent Processing as a new credit card payment method. You'll notice that Ascent is prominently displayed in our payment method and recommended as the go-to option for US merchants.

All other credit card payment methods are still supported - no one was dropped - but Ascent has a great product and is able to set up new merchant accounts right now when some other processors are struggling with COVID-era underwriting requirements. If you had issues with your credit card application being delayed or not approved, look into using Ascent. We have had good luck recently with their team.

The "Setup Done" page at the end of onboarding now links to the Bird's Eye View video in our support docs. Give that a look if you haven't already. It's a great video that shows most of the major areas of the site and what they are used for. We've heard a lot of old users remark how much that has helped even though they've been using OwnerRez for several years. As part of an effort to clean up our marketing and onboarding, we are pushing that video out in several places.

Speaking of marketing, the OwnerRez logo is being normalized everywhere. The login and join pages used to show the old logo, but we've fixed that.

We now support long keys for Stripe. Recently, a number of Stripe users have mentioned that the API keys they are getting from Stripe are longer than the previous standard. We now support up to 128 character keys for Stripe. Hopefully this gives us a few months of breathing room before Stripe changes it up again. 😬

Some OwnerRez users only ever publish and deal in weekly rates. While OwnerRez requires (or at least strongly suggests) that you enter a nightly rate, you don't want those nightly rates showing if you only deal in weekly's. So we added an option to the rate table widget to not show nightly rates even if they technically exist.

The channel rate tester has also gotten some work. As users have started using it, we've had to enhance some things for clarity. If you only have one channel integration configured, the channel rate tester will be pre-selected for that one channel. And we link to your Airbnb tax dashboard now if you're running a Airbnb test. Make sure to look at, and thoroughly read, that Airbnb tax dashboard if you haven't before. It is extremely helpful for seeing your tax situation.

The property ordering page has been enhanced for clarity and accuracy as well. Great feedback on that from everyone!

Channel Bridge has had several more updates. The Dutch (.nl) version of Airbnb is now supported in Channel Bridge, and we also updated the import logic for VRBO bookings to skip bookings with no traveler info.

As usual, users continue to test the flexibility of our widgets! We've gotten great feedback on how properties should be pre-selected if a property key parameter is detected, so we added that. Widgets now support the or_propertyKey parameter and will pre-select the property drop-down if detected.

Hosted websites not showing correct property order. We noticed that our recent property ordering feature was not displaying correct on external websites (such as the properties menu). Not sure how that made it through testing, but it's fixed now!

Accommodation amenity not spelled right. Now fixed. OwnerRez is a giant system with many emails, templates, website, pages and so on. If you run across a misspelled word, please let us know. We like to be accurate but we don't see it all.

Phone number type hiding behind number. When editing guest phone numbers, the mobile/home/work selector was wonky looking. That has now been fixed.

Duplicate inquiries being created. We discovered an issue where some guests with slow internet connections were smacking the "Send Inquiry" or "Book" button on the Book Now widget over and over again because they thought it wasn't working - it was, just slow because of their internet connection. When that happened, 10 or 12 inquiries might be created under the covers. We now show a working indicator and disable the button.

FloridaRentals reporting monthly rates instead of weekly. This has been fixed. No need for you to correct your rates; the API should now push the right indicator.

System alerts not showing right culture (currency/date) format. Depending on where system alerts were sent from, some alerts were reverting back to US-based culture settings and not the user-defined culture settings. This has been fixed.

HI Jennifer, that isn't related to OwnerRez. I've seen that happen to Airbnb messages as well - not sure why/how/what causes that.

I can’t forgive out how to customize the messages for inquiries. I thought I have done it 3 times but it always reverts back. I am

Obviously doing something wrong but don’t know what.

I receive too many phone calls and emails asking questions about the property even though the answers are all posted on my listing.

Happy Friday Everyone!

Florida still can’t make up its mind… Palm Beach County pauses vacation rentals reopening due to growing coronavirus cases. With a safety plan in place and the state’s approval, Palm Beach County had set the stage to let vacation rental owners welcome tourists and staycationers into their dwellings once again. But concerns about a coronavirus resurgence stopped that from going into effect Monday. “It was our hope to begin the opening on June 15th; however, data over the past few days has shown some increases in hospitalization, some increases in percentage of new COVID-19 cases over the past weeks and a bump in influenza-like illnesses in our emergency rooms,” read a statement on the county’s website. Sigh.

On Tuesday, short-term vacation rentals are allowed to resume most operations on Maui, the Big Island and Kaua'i. Owners are not allowed to rent to anyone who is undergoing quarantine. Honolulu Mayor Kirk Caldwell has yet to submit a request to Governor David Ige to allow legal short-term vacation rentals to operate on O'ahu.

If you’re a traveler, watch out for rental fraud! Investigations are ongoing in at least three cases of rental fraud that have occurred in the last month in Holmes Beach, Florida. Visitors arrived only to find out that they really didn’t have a booking at the property they thought they’d reserved. Now Holmes Beach police officers are warning rental owners to be on the lookout for any fraudulent advertisements for their properties, and are warning visitors to be careful how they book their next vacation.

There’s an interesting case going on in the Outer Banks. A large PM is under scrutiny after reneging on an alleged promise to refund money. Dozens of guests reported the PM and now North Caroline state is investigating.

What’s particularly interesting is that the NC Real Estate Commission evidently mandates certain refund policies. Notice this line:

"If you have a contract that cannot be performed, it's not a contract, and you're due your money back," Stein [NC Attorney General] said. "We are in the process of digging into this and investigating it, and if what we find out leads us to conclude that these people are in the legal wrong and they need to pay these people back we will do whatever necessary to get these customers their money back."

What if the signed contract stated that no refunds are given for cancellations or ‘acts of god’, and the guest knew and signed to that? Does that matter? Shouldn’t the contract hold up?

COVID-19 has caused a huge downturn in rental revenue but 1 bad guest can create expenses that are totally unexpected.

We're thinking about a number of different upcoming needs at the moment, and it's quite possible that customer support might lead into those in time. So we'd be glad to consider a wide range of experience and backgrounds. With a small, fast-growing company, you never know where you may find a good fit!

OwnerRez is an incredibly powerful tool that does a lot of high level tasks automatically. But there are still some thing that take time. We'd like to hear what repetitive task you think takes the most time to do in OwnerRez.

What do you find yourself doing over and over again?

(make sure to scroll to the bottom and click the Submit button)

If the survey form didn't load, use this link instead:

What repetitive task takes you the most time in OwnerRez each week?

Great idea to recruit from your users! Any idea of a salary/hourly range? This isn't something I can take on, but I know a few people who may be good but make it a policy not to share job opportunities that don't publish a salary/hourly range.

Thanks!

I don't know if this is a bug or even related to OwnerRez but I have received two messages in my Airbnb inbox (on airbnb) and I cannot make the unread notification (dot) go away no matter how many times I open the messages. It seems to have happened since OwnerRez began showing the Airbnb inbox. Is this connected or just coincidence?

Would love to be a part of OwnerRez!!! Just listed our PCB rental with you guys and are excited for the opportunities it will bring...I manage a VA clinic and also am over QA at the clinic. Will send my info:)

Lisa Lansdell